After a record-breaking 2021, global digital health investment continues its slowdown in Q2’22.

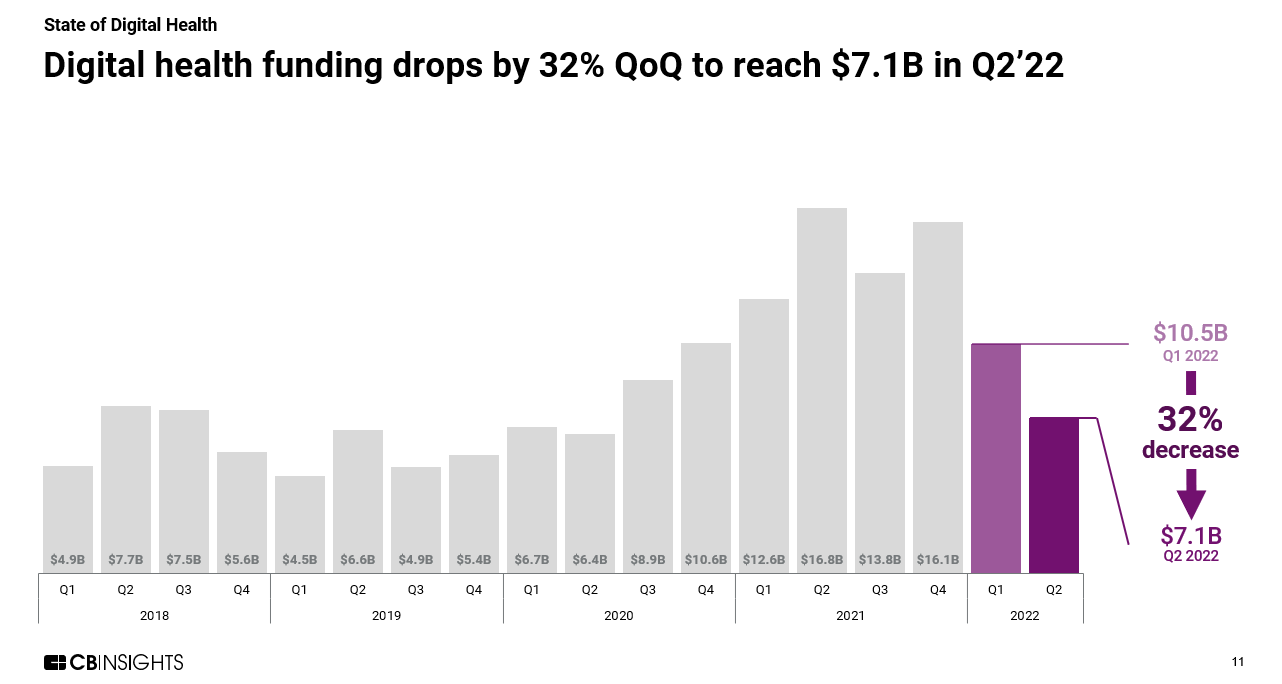

Global digital health funding reached $7.1B in Q2’22 — down 32% from the previous quarter, continuing the decline from record highs in 2021. The decrease in funding and deals affected almost all sectors across digital health except for Health IT, mirroring the broader downtrend in venture funding.

Below, check out just a few highlights from our 197-page, data-driven State of Digital Health Q2’22 Report. For deeper insights, all the record figures, and a boatload of private market data, download the full report.

Q2’22 highlights across the digital health ecosystem include:

- Amid a global funding slump, Europe was the only region to see a QoQ increase in funding, boosted by Alan‘s $193M Series E mega-round.

- By region, the US raised the most in total digital health funding in Q2’22 ($4.8B), despite a 53% YoY decline.

- Total digital health unicorns broke 100 for the first time ever, even as unicorn births held steady QoQ. New entrants include Oura ($2.6B valuation), Clarify Health ($1.4B), and Biofourmis ($1.3B).

- After a slight recovery in Q1’22, M&A exits saw their most dramatic drop of the last year, falling to 83 deals — on par with 2020 M&A levels. The digital health space also saw only 1 IPO in Q2’22: Heart Test Laboratories.

- Gaingels and Insight Partners emerged as the most active digital health investors of the quarter, backing 9 companies each, followed by General Catalyst with 7.

Download our Q2’22 State of Digital Health Report to learn more about all these trends and more.

If you aren’t already a client, sign up for a free trial to learn more about our platform.