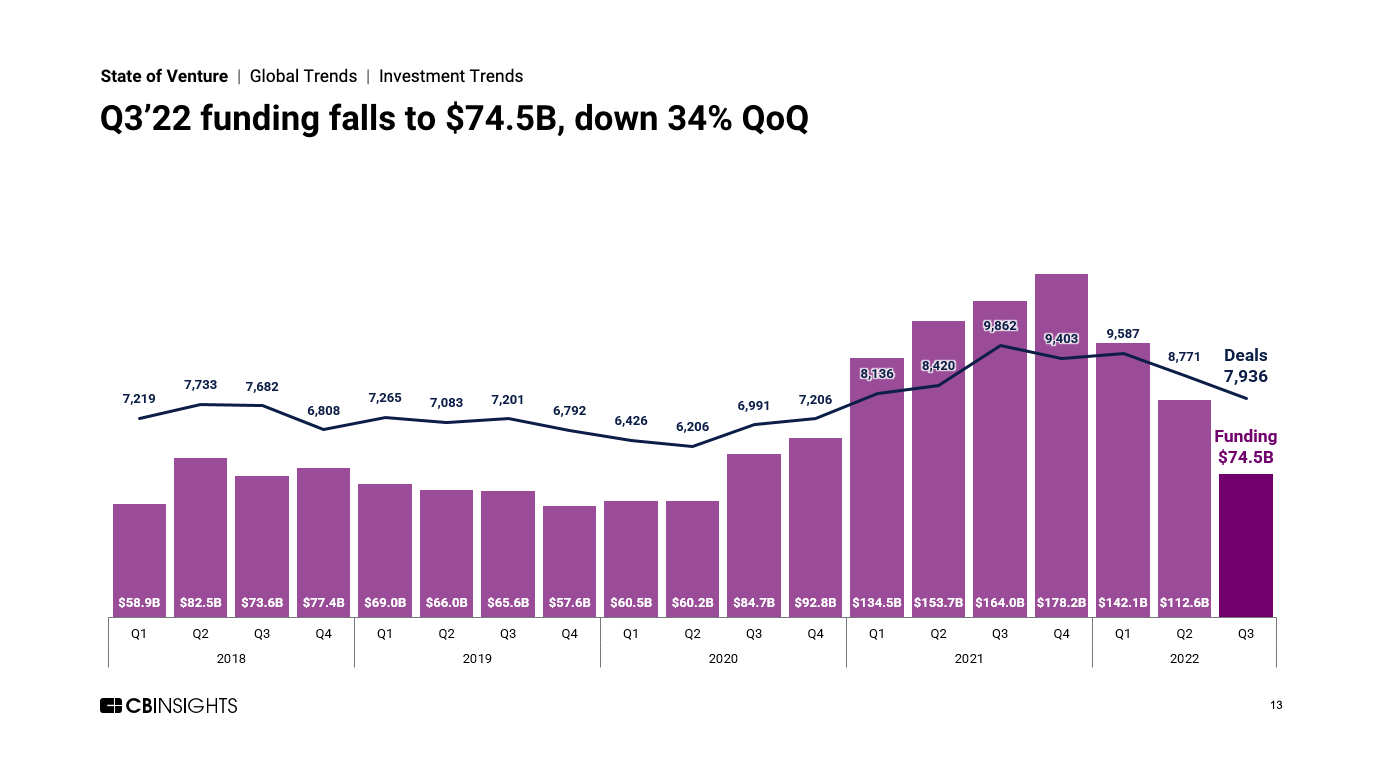

The global venture ecosystem continues its slowdown in Q3’22 as funding decreases 34% quarter-over-quarter.

Global venture funding reached $74.5B in Q3’22, hitting a 9-quarter low. This represented a 34% drop quarter-over-quarter (QoQ) — the largest quarterly percentage drop in a decade — and a 58% decline from the investment peak reached in Q4’21.

The number of deals fell to 7,936 total, marking a 10% quarterly drop.

US-based companies accounted for just under half (49%) of global funding in Q3’22, collectively raising $36.7B across 2,866 deals. Some of the largest rounds in the US went to TerraPower, EnergyX, and Xpansiv.

Other Q3’22 highlights across the venture ecosystem include:

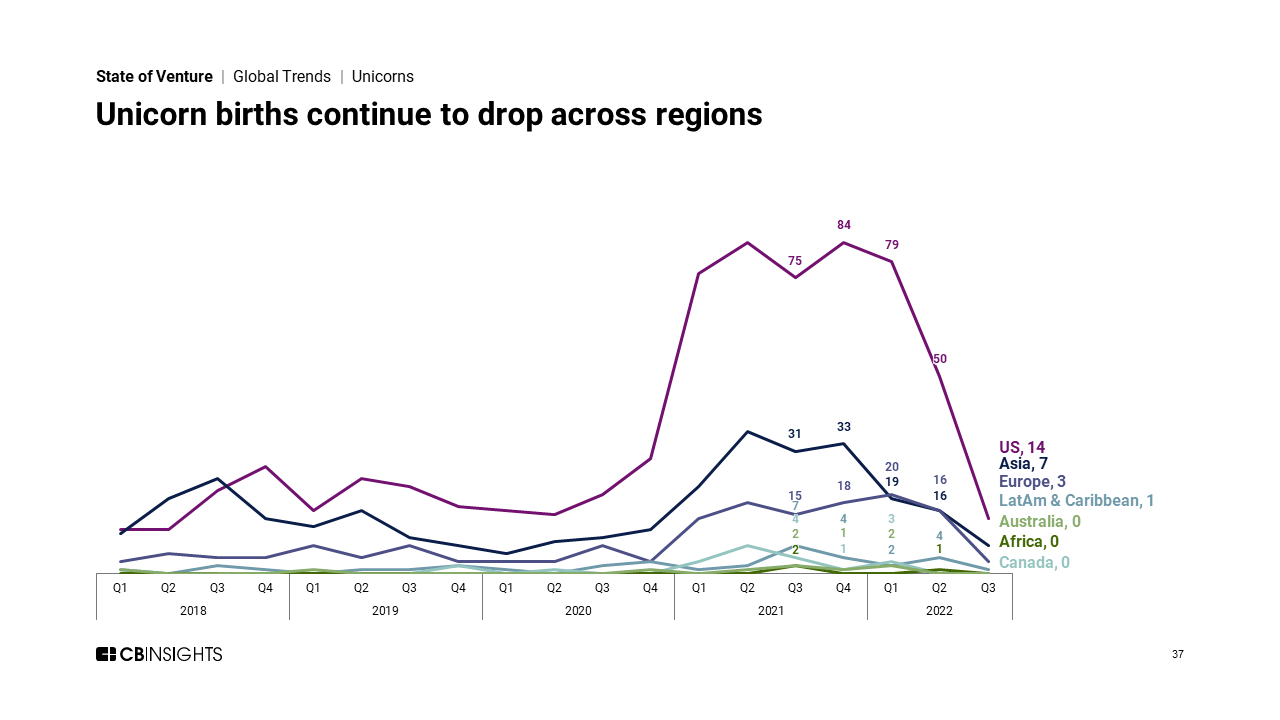

- Q3’22 saw only 25 new unicorns (private companies valued at $1B+) — the lowest unicorn birth count since Q1’20. The US accounted for the majority (14) of these births.

- $100M+ mega-rounds collectively accounted for $29.6B in Q3’22, marking a 9-quarter low and a 44% drop QoQ.

- Retail tech funding declined 33% QoQ to $8.5B, even as deals ticked up 5% to 776. The average deal size for the space in 2022 YTD reached $24M, down 35% compared to 2021 averages.

- The fintech sector also continued to contract. With $12.9B raised across 1,160 deals, Q3’22 was the weakest quarter the sector has seen since Q4’20.

- Global digital health deals fell to their lowest level in years, with $4.6B raised across just 427 deals. The US led, accounting for more than half of total digital health funding at $3B.

- Last quarter’s top 3 investors, Tiger Global Management, Gaingels, and SOSV, accounted for 109 investments in Q3’22 — less than half the amount they made in Q2’22. Tiger Global Management was not among the top ten investors after leading the list for 3 consecutive quarters.

Download our Q3’22 State of Venture Report to learn more about all these trends and more.

If you aren’t already a client, sign up for a free trial to learn more about our platform.