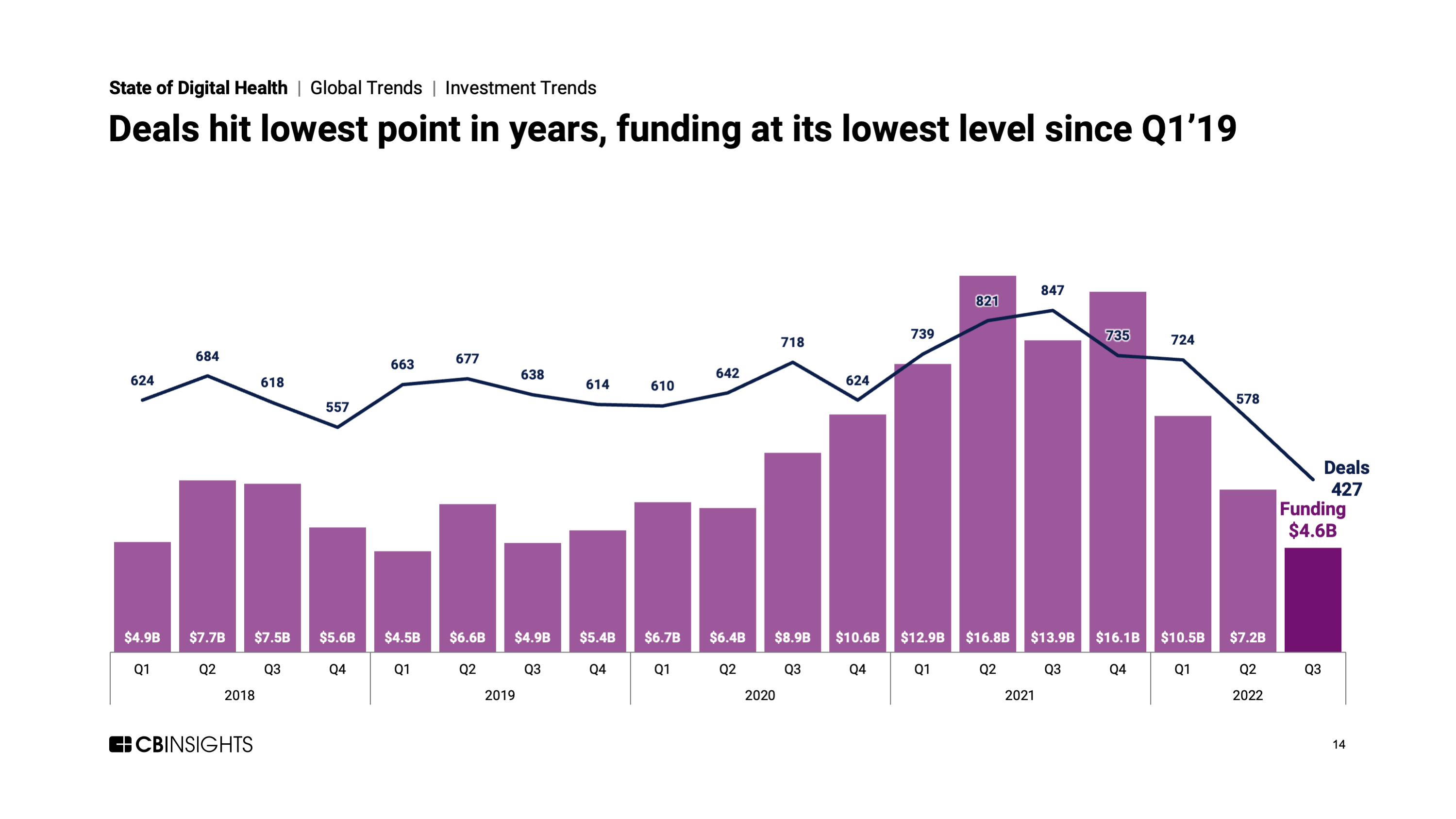

The global digital health market continues its decline in Q3’22 as funding decreases 36% quarter-over-quarter.

Global digital health funding reached $4.6B in Q3’22, its lowest total since Q1’19. This marks the 3rd straight quarter with a decline of at least 30% and a 72% decline from the quarterly investment peak seen in Q2’21.

The number of deals dropped for the 4th consecutive quarter to 427, the lowest quarterly total in more than 5 years.

US-based companies raised $3B in Q3’22. From a deals perspective, the US led with 233 deals — more than all the other regions combined. Some of the largest rounds in the US went to companies including ArsenalBio, Alma, and Senda Biosciences.

Other Q3’22 highlights across the digital health market include:

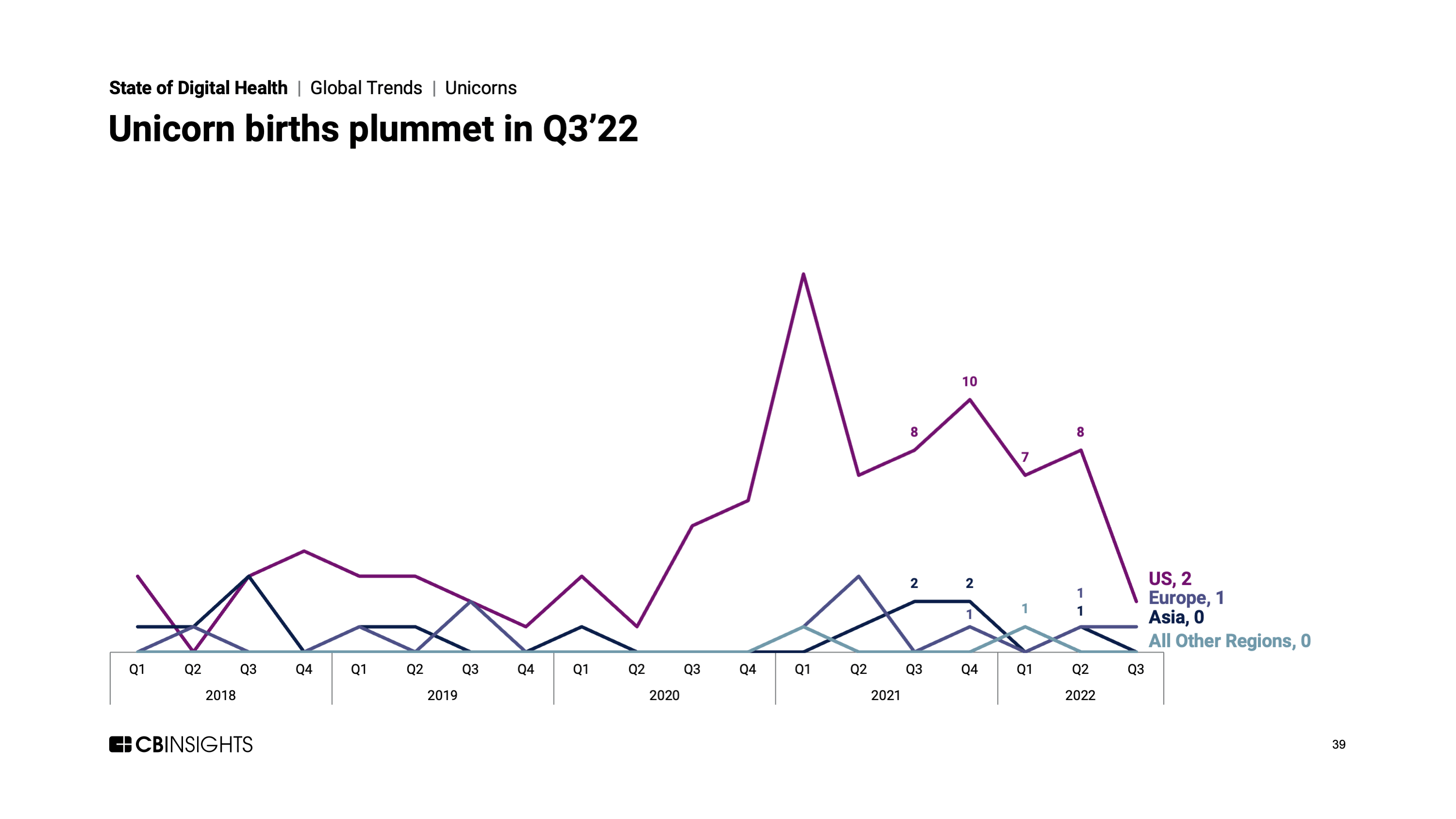

- Q3’22 only saw 3 new unicorns (private companies valued at $1B+) — the lowest unicorn birth count since Q2’20.

- Funding from $100M+ mega-rounds declined for the 3rd consecutive quarter to $1.2B — the lowest level since Q1’19.

- Mental health tech funding rebounded slightly from Q2’22, reaching $0.7B after 2 straight quarters of decline.

- Funding to Asia-based companies fell by 18% to $0.9B. However, the region’s 6 IPO exits in Q3’22 represent its 3rd highest quarterly total for the past 5 years.

- Last quarter’s top investors, General Catalyst, Lightspeed Venture Partners, ARCH Venture Partners, and Transformation Capital tallied up 20 investments in Q3’22 — down 20% from Q2’22 and 46% from Q1’22.

Download our Q3’22 State of Digital Health to learn more about all these trends and more.

If you aren’t already a client, sign up for a free trial to learn more about our platform.