Energy tech funding and deals continue to fall but remain elevated relative to recent years.

Global energy tech funding dropped for the second straight quarter to hit $7.5B in Q2’22. While this marked a 24% quarter-over-quarter (QoQ) decline, funding was only down 3% year-over-year (YoY) and remained elevated compared to pre-2021 levels. Similarly, deal count also took a QoQ hit but stood as the fourth-highest figure in recent years.

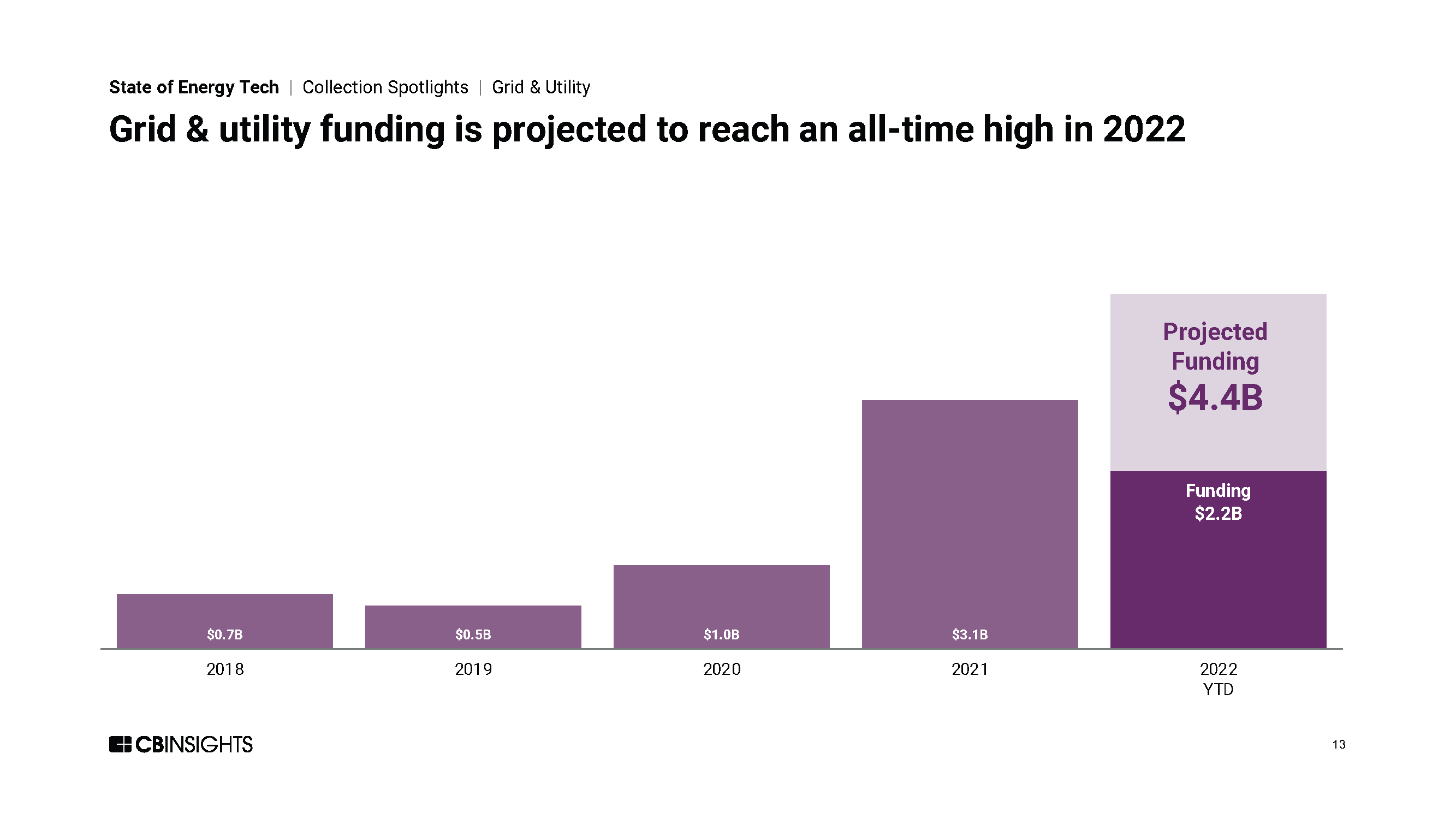

In contrast to the broader funding free fall in energy tech and beyond, the grid & utility sector saw funding rise to reach 2021’s year-end total ($2.2B) just halfway through 2022. The largest rounds in the space went to Agilitas Energy ($350M), Arcadia ($200M), and Mainspring Energy ($150M).

Below, check out a few highlights from our 159-page, data-driven State of Energy Tech Q2’22 Report. For deeper insights, all the record figures, and a boatload of private market data, download the full report.

Q2’22 highlights across the energy tech ecosystem include:

- China-based companies saw funding fall 52% QoQ to reach $348M, marking a 91% decline from the record $3.9B raised in Q3’21.

- A record amount of funding flowed into the oil & gas tech space, on the other hand, with startups raising $1B across 24 deals.

- Quarterly $100M+ mega-round funding declined for the third consecutive quarter to hit $4.5B, a 55% drop from its $9.9B peak late last year.

- While oil & gas tech mid- and late-stage deal share grew in the first half of 2022, early-stage deal share was down 11 percentage points from last year and 24 from its 2019 heyday.

- Seven new energy tech unicorns (nearly one-third of the total herd) were born in Q2’22. The unicorn club now includes Beta Technologies ($2.4B valuation), Crusoe ($1.8B), and Arcadia ($1.5B).

Download our Q2’22 State of Energy Report to learn more about all these trends and more.

If you aren’t already a client, sign up for a free trial to learn more about our platform.