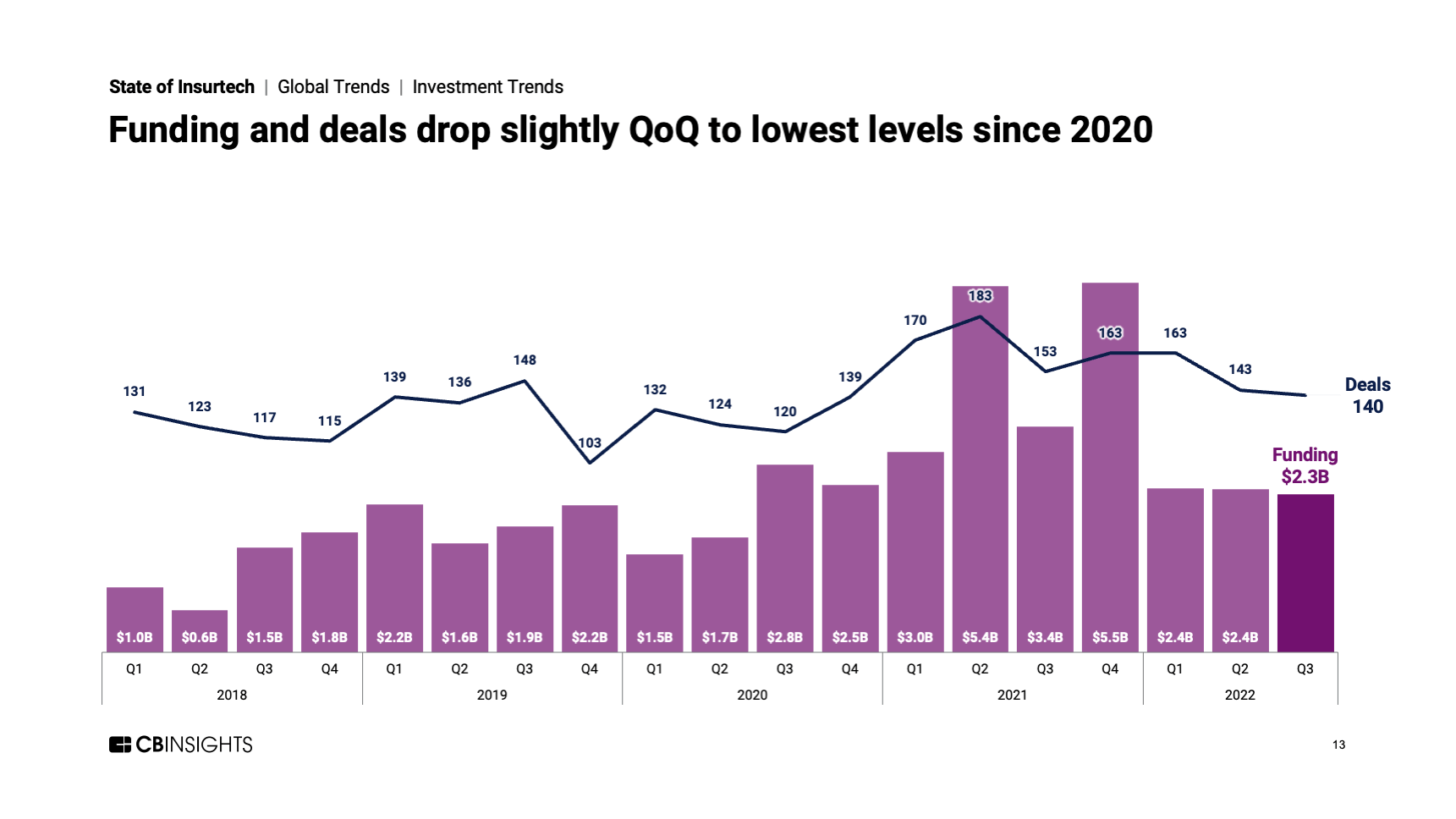

Insurtech investment activity lags the record highs of 2021, but remains nearly steady quarter-over-quarter.

Insurtech funding dipped by just 4% quarter-over-quarter (QoQ) in Q3’22 to hit $2.3B — the lowest it’s been since Q2’20. Deals also fell slightly, down 2% QoQ to reach 140.

Funding was primarily driven by P&C insurtech startups, which grabbed $1.8B across 89 deals — representing over 75% of all insurtech funding in Q3’22.

Below, check out a handful of highlights from our 82-page, data-driven State of Insurtech Q3’22 Report. For deeper insights, all the record figures, and a ton of private market data, download the full report.

Other Q3’22 highlights across insurtech include:

- Mega-round funding came in at $1.5B, representing over 60% of all insurtech funding.

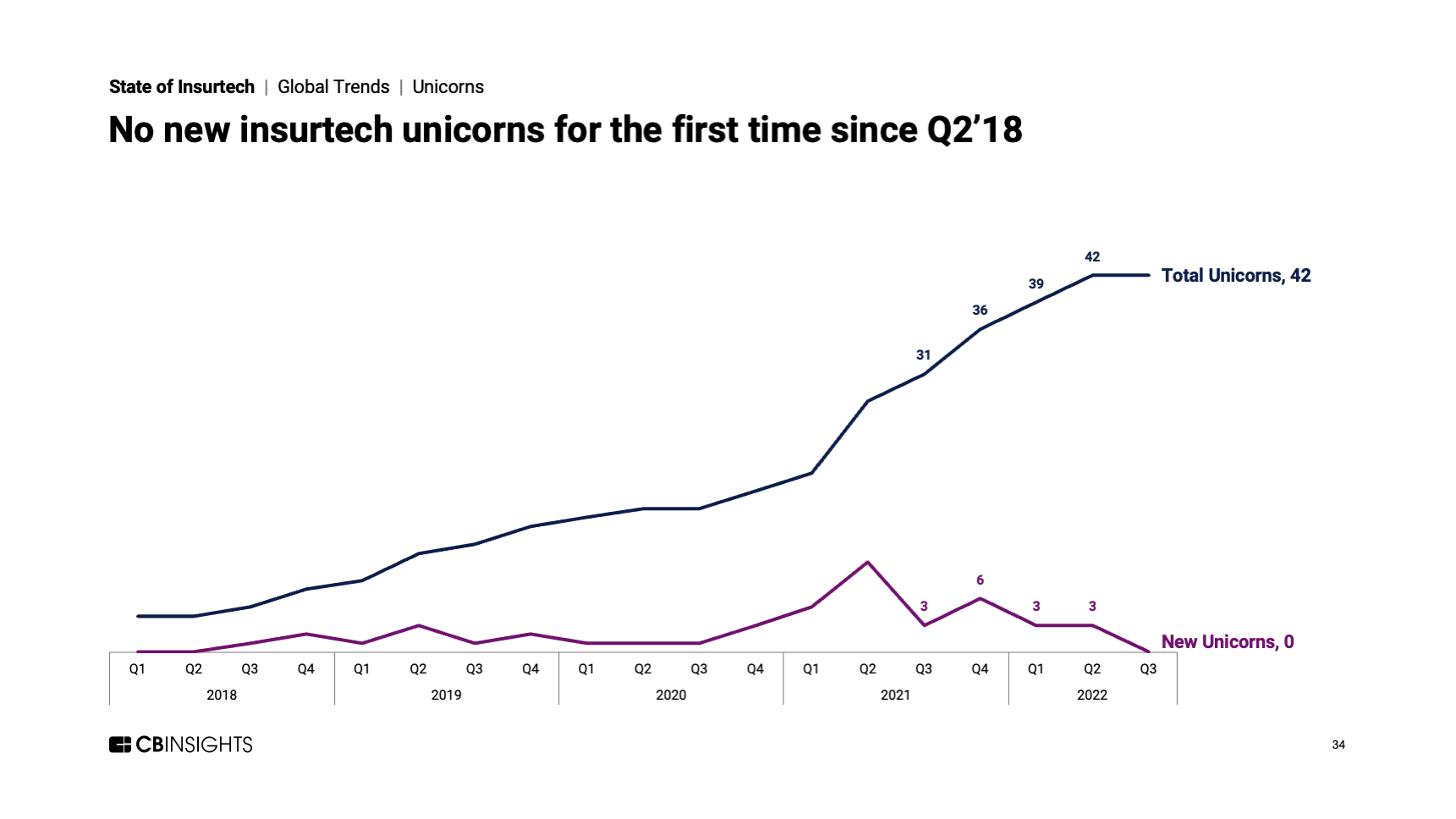

- For the first time since Q2’18, there were no new insurtech unicorn births.

- In 2022 so far, average and median deal sizes are down 35% and 29%, respectively, compared to FY 2021’s totals.

- Asia (25%) surpassed Europe (21%) in deal share for the first time since Q4’21.

- After 4 quarters of decline, P&C insurtech saw funding grow 20% QoQ.

- Anthemis was the most active insurtech investor, backing 4 companies in Q3’22. Eos Venture Partners, Greycroft, Lerer Hippeau, and SiriusPoint were tied for second, each with 3 companies backed.