Global corporate venture capital activity continues to slow in Q1'23, with funding dropping 12% QoQ.

Global corporate venture capital (CVC)-backed funding and deals continued on their declines in Q1’23. However, median early-stage deal size hit a record high, and $100M+ mega-round funding jumped by 28% quarter-over-quarter (QoQ).

Using CB Insights data, we highlight some of the key takeaways from our Q1’23 State of CVC Report, including:

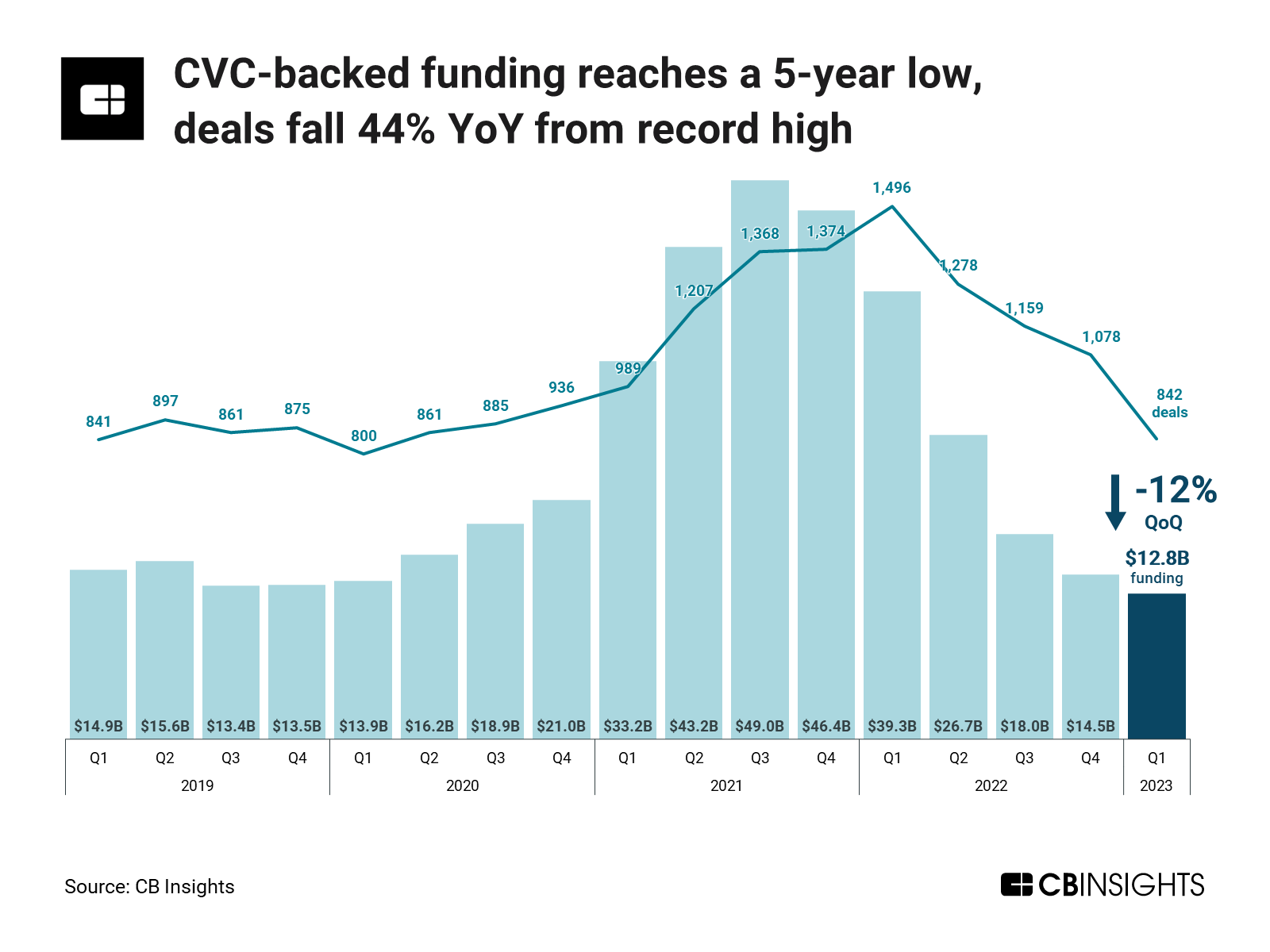

- Global CVC-backed funding reaches a 5-year low, deals fall 44% year-over-year (YoY) from record high.

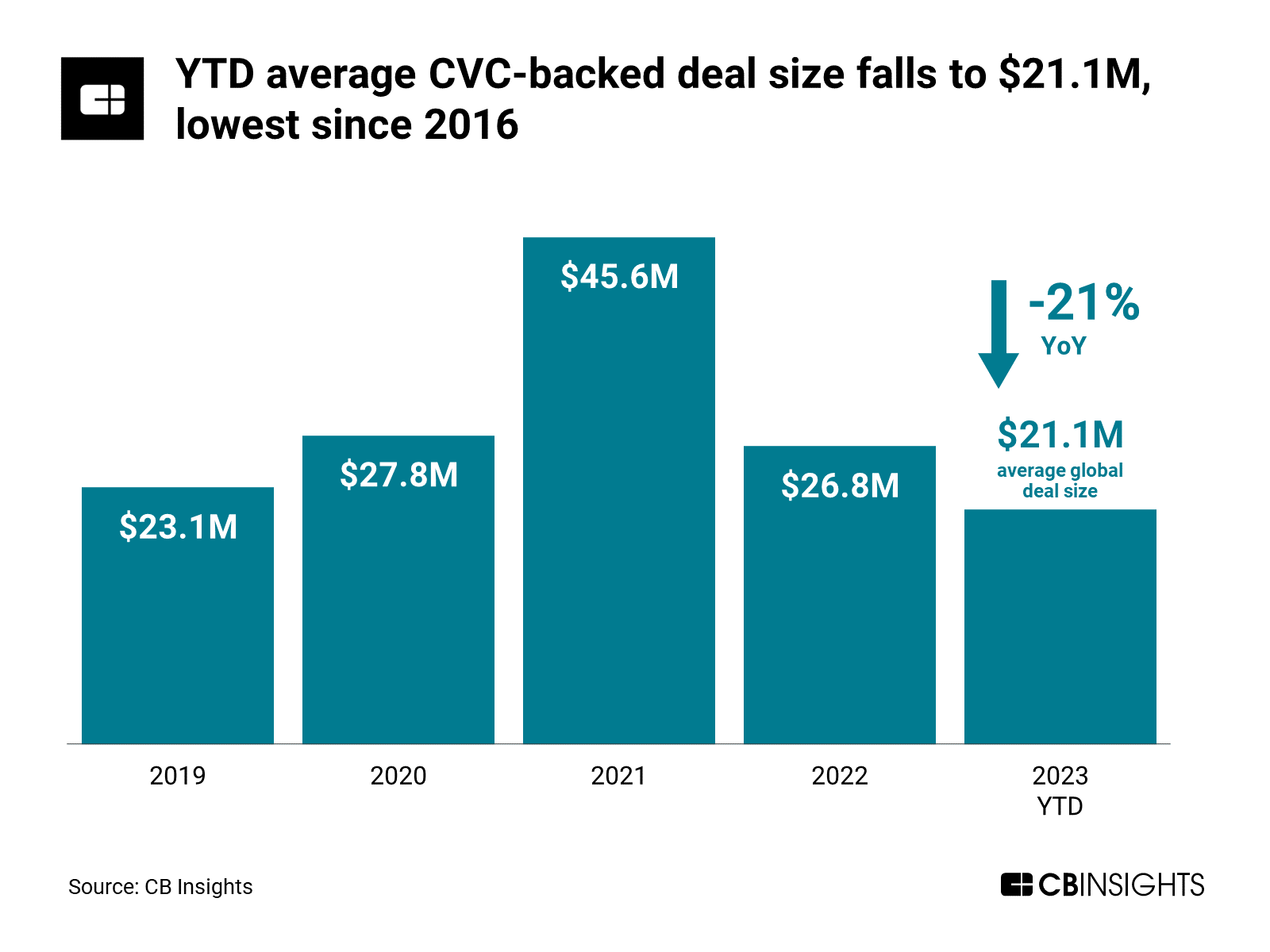

- Average deal size falls to $21.1M in 2023 YTD, lowest since 2016.

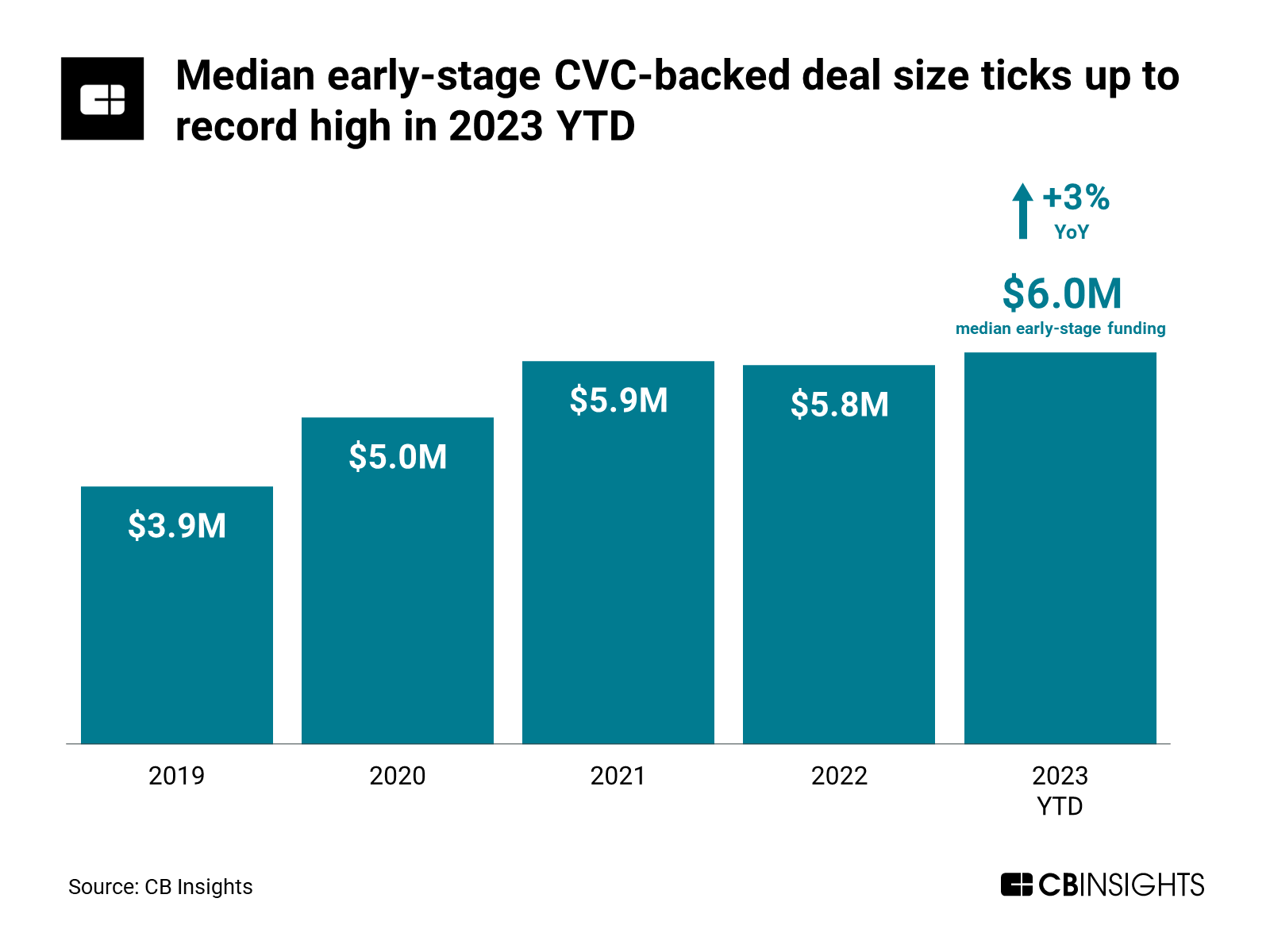

- Median early-stage CVC-backed deal size ticks up to record high.

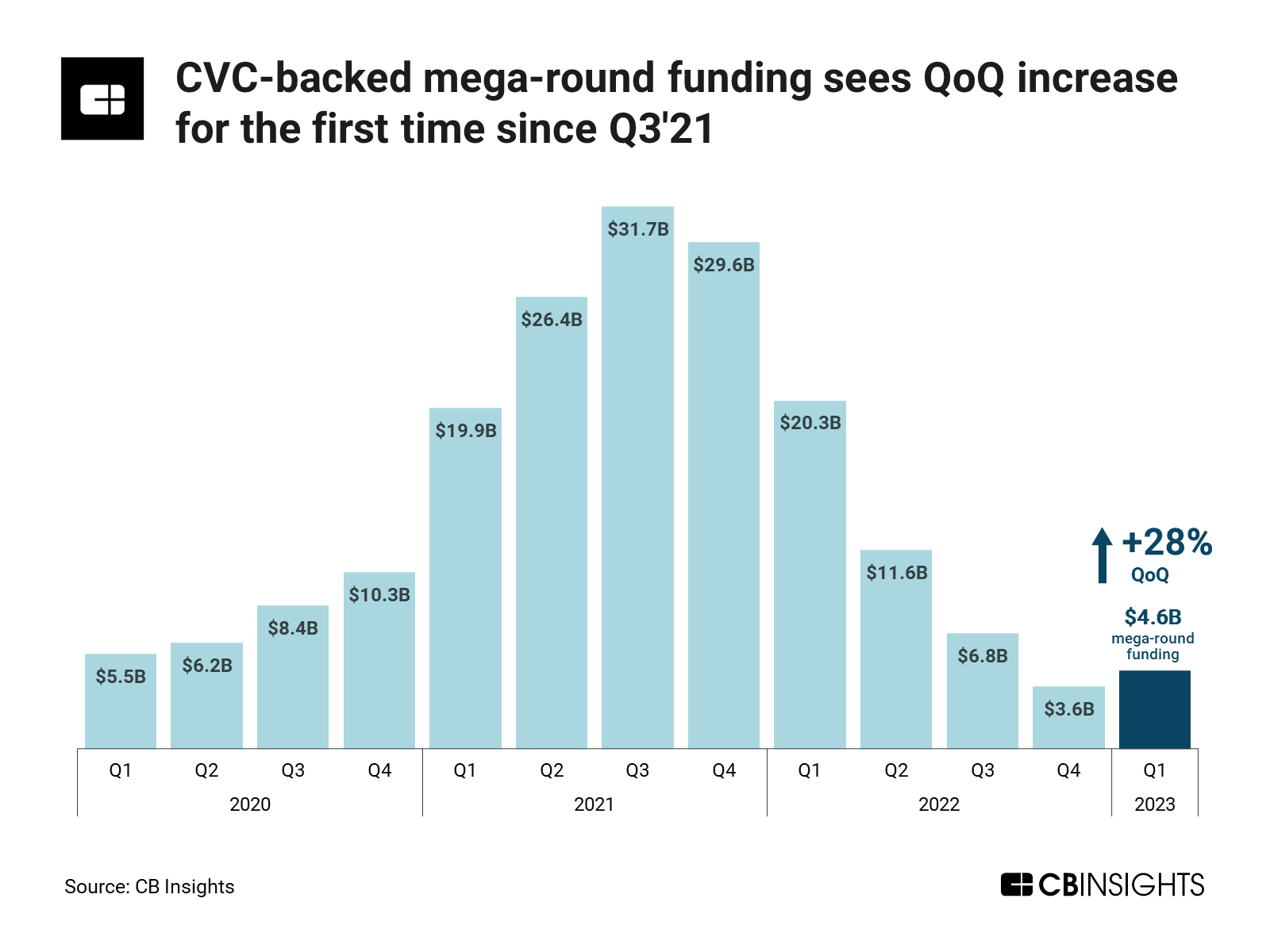

- $100M+ mega-round funding sees QoQ increase for the first time since Q3’21.

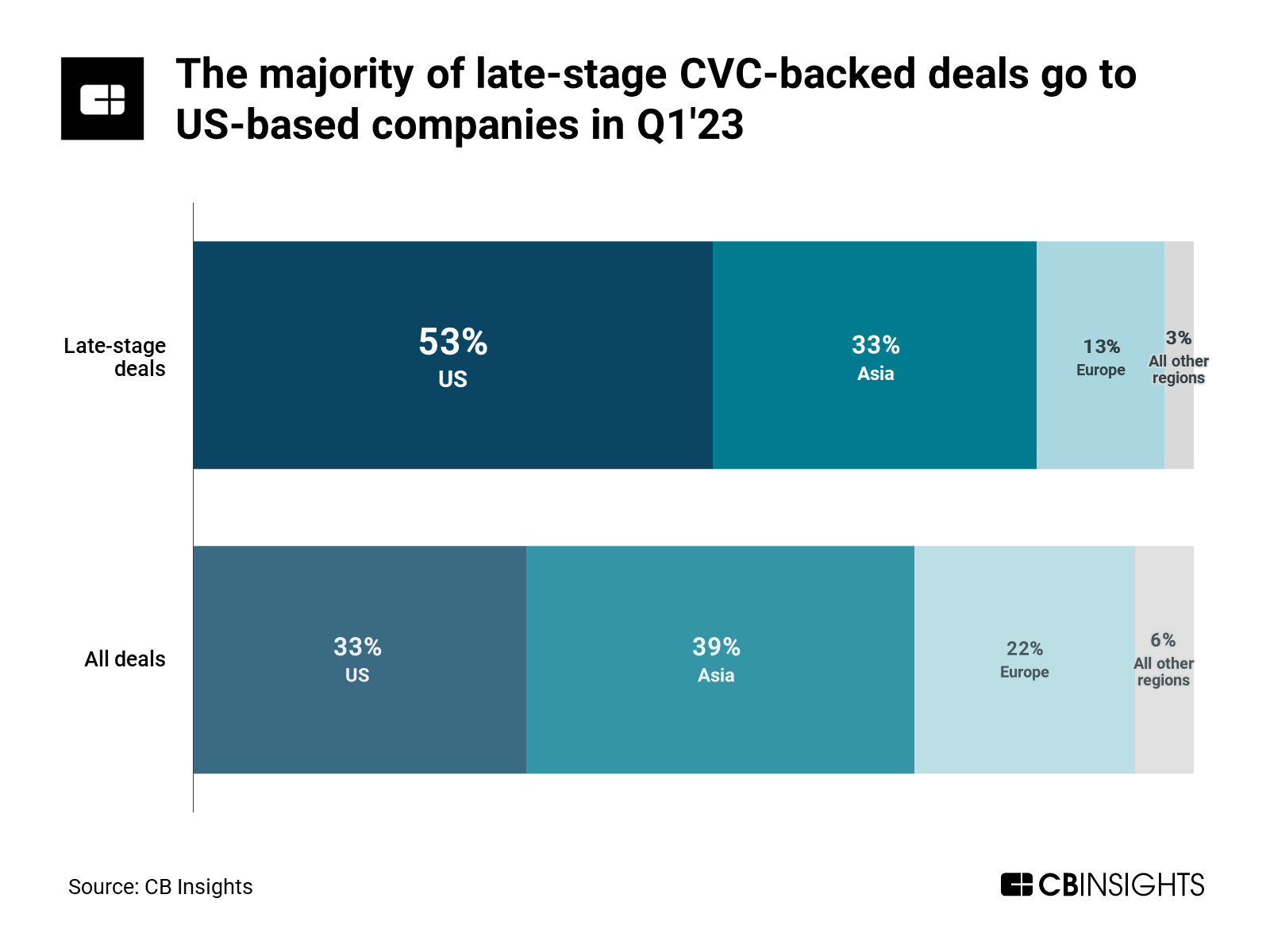

- The US sees the majority of late-stage CVC-backed deals in Q1’23.

CB Insights clients can see all the latest investment data by signing in and downloading the full State of CVC Q1’23 Report using the sidebar.

Let’s dive in.

Global CVC-backed funding fell 12% QoQ, from $14.5B in Q4’22 to $12.8B in Q1’23. This marked the lowest quarterly funding level since Q1’18, which saw $11.8B. The decline in CVC-backed funding aligned with the broader drop in global venture funding, which fell 13% QoQ.

Deals with CVC participation dropped 22% QoQ, dipping below 1,000 for the first time since 2021. Global CVC-backed deal count was also down 44% YoY, from a record high of 1,496 in Q1’22.

Average CVC-backed deal size came in at $21.1M in 2023 YTD, down from $26.8M in full-year 2022. This represents the lowest average deal size since 2016, when it stood at $19.1M.

Nevertheless, the broader venture funding environment saw a greater percentage drop (-25%) in average deal size than CVC.

Median CVC-backed deal size also dropped, falling from $10M in 2022 to $8.8M in 2023 YTD. In line with this trend, median late-stage CVC-backed deal size fell from $87M to $50M over the same period.

Despite the drop in median CVC-backed deal size, the median early-stage CVC-backed deal size ticked up to a record high of $6M in 2023 YTD. This was the only deal stage to see an increase in median deal size from full-year 2022 to 2023 YTD.

Notably, median early-stage CVC-backed deal size managed to increase while the median deal size of early-stage deals in the broader venture arena decreased by 8%. CVC-backed deals also continued to command larger median deal sizes than venture deals overall in 2023 YTD.

In comparison to venture deals more broadly, median CVC-backed deal size was up:

- 2.7x for early-stage deals

- 1.3x for mid-stage deals

- 3.3x for late-stage deals

CVC-backed mega-round funding and deals rose for the first time since Q3’21, increasing 28% and 8% QoQ, respectively. Mega-round funding’s share of total CVC-backed funding also climbed, jumping 11 percentage points QoQ to reach 36% in Q1’23.

Total global venture mega-round funding, on the other hand, fell 8% to reach a 6-year low in Q1’23.

Mega-round activity was particularly strong across CVC-backed Series B and C deals in Q1’23. The top 10 CVC-backed Series B deals in Q1’23 were mega-rounds, as were 7 of the top 10 Series C deals.

US-based companies saw $7.6B in CVC-backed funding in Q1’23, equivalent to 59% of all global funding. While US CVC-backed funding remained flat QoQ, the region’s share of global deals increased by 2 percentage points.

The US’ share of late-stage CVC-backed deals experienced an even greater jump, climbing 13 percentage points QoQ. Startups based in the country secured 6 of the top 10 Series D deals and all of the top 10 Series E+ deals.

Additionally, US-based companies accounted for the top 3 CVC-backed equity deals overall in Q1’23. Notably, these deals were all mid-stage deals:

- Monogram Health – $375M Series C

- Adept – $350M Series B

- Our Next Energy – $300M Series B